Rival as model

Since its creation in 1905, Hydro has occupied a key position in Norwegian industry with such activities as fertiliser production and aluminium processing. It became involved in the oil sector as early as the 1960s. When the Norwegian government was deciding how this new industry should be organised, Hydro therefore represented a clear candidate for the state’s main commercial instrument. A majority shareholding in the company was acquired by Per Borten’s government. However, this non-socialist coalition had to resign in 1971 as a result of internal disagreements over European Community membership.

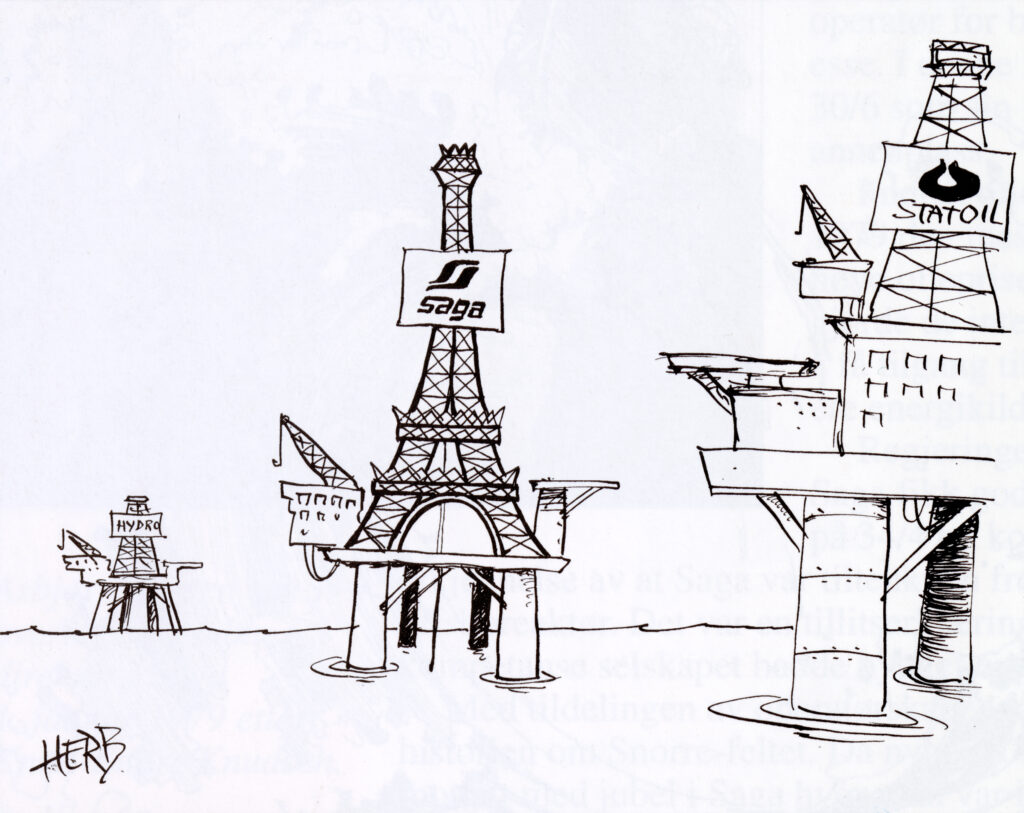

The subsequent Labour government headed by Trygve Bratteli proposed the creation of a new oil company wholly owned by the state. Statoil thereby saw the light of day in 1972 and became the dominant Norwegian oil company. Along with privately owned Saga Petroleum, it and Hydro performed a politically managed balancing act between state control and private initiative on the Norwegian continental shelf (NCS) for more than a quarter of a century.

Large and lucrative interests in production licences were awarded to each of these three companies during the 1970s and into the 1980s. But the number of new, extremely profitable fields discovered fell as time passed. Combined with a slump in oil prices from 1986, this helped to reduce some of the government’s protectionist scope. Unless the favourable treatment meted out to domestic companies was modified, foreign companies might decide it was no longer worth operating on the NCS. The government did not want such involvement to reduce because it spread exploration risk when project profitability was less assured than before.

Hydro as a model

In these circumstances, the Statoil management began to question the benefit of being wholly state-owned. It noted on a number of occasions that Hydro had a more advantageous ownership structure. The company was Statoil’s biggest competitor on the NCS and in a much freer position to take decisions on the basis of commercial assessments. Moreover, the European Economic Area (EEA) agreement which came into force in 1994 helped to reinforce and formalise requirements for (international) competition on commercial terms.

Statoil CEO Harald Norvik was a prominent exponent of taking Hydro’s ownership structure as a model for his company as well.[REMOVE]Fotnote: Thomassen, Eivind, 2020, The Crude Means to Mastery. Norwegian National Oil Company Statoil (Equinor) and the Norwegian State 1972-2001, PhD thesis, University of Oslo: 205. “In Hydro, the state was a heavyweight, long-term, clear and respected owner, but the company’s presence on the stock exchange meant that [it] became normalised – measured and weighed in the same way as its competitors,” Harald Norvik has observed.[REMOVE]Fotnote: Harald Norvik interviewed in 25 April 2017, quoted in Storsletten, Aslak, 2018, Prosessen bak delprivatiseringen av Statoil i 2001 – fra selskap til vedtak, master’s thesis, University of Oslo: 31.

Another aspect of full state ownership which the Statoil management felt acted as a restraint was the government’s dividend policy. On a number of occasions, it took large pay-outs from the company for budgetary reasons. That affected operational predictability.[REMOVE]Fotnote: Storsletten, Aslak, op.cit: 73.

Hydro gives voice

However, Hydro was not only an inspiration for the Statoil management as a suitable form of state ownership. It also had a voice in Statoil’s actual privatisation process during 1999-2001.

After Hydro and Statoil had jointly taken over Saga in 1999, they remained the two large domestic players on the NCS. It was therefore not unnatural that the Ministry of Petroleum and Energy asked Hydro in June 1999 to “provide its views on shaping state involvement in petroleum operations on the NCS”. This request was made in connection with preparing a proposition (Bill) on ownership of Statoil and the future management of the state’s direct financial interest (SDFI) in the oil sector.[REMOVE]Fotnote: Hydro’s consultation response, see appendix 3, pages 180-187, to Proposition no 36 (2000-2001) to the Storting (parliament), Norsk Hydros vurdering av det statlige engasjement i oljevirksomheten – Brev fra Norsk Hydro av 1. september 1999. https://www.regjeringen.no/contentassets/712e1fc123f84e3ea21368770360596d/no/pdfa/stp200020010036000dddpdfa.pdf

Hydro took this opportunity to support a partial privatisation of Statoil, since this would “mean that it will be easier to compare the development of the two companies in relation to the criteria given emphasis by the stock market”.[REMOVE]Fotnote: Ibid: 181, 187 The company also made proposals concerning more efficient management of the SDFI.

The latter was the result of a cross-party compromise in 1984, when the state took direct control of a substantial part of Statoil’s cash flow – income and expenses – in a process known as “wing-clipping”. Since then, Statoil had been responsible for managing the SDFI on behalf of the government.

Thanks to the partial privatisation process, this arrangement was now in play and Hydro had a clear interest in positioning itself to exert the greatest possible influence over the formula for a possible transfer of SDFI assets to private players. It argued that the government was losing “potential added value which could be created through a more commercial management”.[REMOVE]Fotnote: Ibid: 183

At the same time, it was important for Hydro to warn against acceding to the Statoil board’s proposal that the company should acquire the whole SDFI. This would “mean such as substantial shift in the relative sizes of Statoil and Hydro that a basis would no longer exist for equal competition between the two milieus. Unless an arrangement is established for transferring SDFI interests which also gives Norsk Hydro an opportunity to participate in the process, the company’s role as an active competitor and agenda-setter on the NCS could be gradually weakened”.[REMOVE]Fotnote: Ibid: 184

The decision

Through its response to the consultation on Proposition no 36, Hydro had gained a broad opportunity to support a partial privatisation of Statoil while positioning itself in relation to the SDFI. This proposition in turn provided the basis for consideration by the standing committee on energy and the environment in the Storting (parliament) and its recommendation in favour of partial privatisation.[REMOVE]Fotnote: Recommendation no 198 (2000-2001) to the Storting, Innstilling fra energi- og miljøkomiteen om eierskap i Statoil og fremtidig forvaltning av SDØE, https://www.stortinget.no/no/Saker-og-publikasjoner/Publikasjoner/Innstillinger/Stortinget/2000-2001/inns-200001-198/ The Storting voted in line with this recommendation on 26 April 2001.[REMOVE]Fotnote: Storting proceedings, 26 April 2001, https://www.stortinget.no/no/Saker-og-publikasjoner/Publikasjoner/Referater/Stortinget/2000-2001/010426/2

According to that decision, a dedicated state-owned company – given the name Petoro – was to be established to manage the great bulk of the SDFI portfolio. However, about 20 per cent of these assets were sold to other players, primarily Statoil and Hydro with about 75 and 25 per cent respectively.

The partial privatisation process left Statoil more similar to Hydro in terms of state ownership.

A few years later, Hydro’s oil and energy interests would be merged with Statoil.

arrow_backÅsgard – a technological quantum leapBackground for the partial privatisationarrow_forward